The coronavirus pandemic has burdened many companies with adverse financial conditions, including a significant reduction of revenue and cash flows, a need for liquidity, increased leverage, and employee layoffs and furloughs.

As a result, many companies had to raise capital and liquidity through the debt and equity markets, while others face financial distress that may ultimately lead to bankruptcy and reorganization. Entities that enter Chapter 11 bankruptcy protection in the United States need to develop, negotiate, and confirm a plan of reorganization with their creditors and the bankruptcy court. As part of Chapter 11 proceedings, the debtor must prepare for review and approval of various documents including, but not limited to, disclosure statements, interim financial statements, business plans of core and noncore operations with details of financial projections, valuation analyses that will form the basis of the “reorganization value,” and a liquidation analysis.

Going through the bankruptcy process requires specialized knowledge and experience with valuation, accounting, tax, and legal matters.

The reorganization plan: (1) divides the creditors into classes based on the nature of their claims; (2) proposes treatment of each class of claims; and (3) provides the means for the execution of the plan, the goal of which is to ultimately repay the creditors, at least in part, and to have the successor entity be a viable going concern entity. The reorganization plan may involve restructuring of the existing debt, sale of assets, issuance of new instruments, infusion of new investors, or a merger with another entity.

As an entity moves through the bankruptcy process, it must meet certain criteria to qualify, upon emergence, for fresh-start reporting under FASB ASC Topic 852, Reorganizations. Such criteria include the loss-of-control test and the reorganization-value test.

Under the loss-of-control test, Paragraph 852-10-45-19 requires that “holders of existing voting shares immediately before confirmation receive less than 50 percent of the voting shares of the emerging entity” and that “[t]he loss of control contemplated by the plan must be substantive and not temporary. That is, the new controlling interest must not revert to the shareholders existing immediately before the plan was filed or confirmed.” If this does not occur, then the emerging entity does not qualify for fresh-start reporting.

Under the reorganization-value test, Paragraph 852-10-45-19 requires that the reorganization value of the assets of the emerging entity immediately before the date of confirmation be less than the total of all post-petition liabilities and allowed claims. Topic 852 defines reorganization value as “[t]he value attributed to the reconstituted entity, as well as the expected net realizable value of those assets that will be disposed of before reconstitution occurs. Therefore, this value is viewed as the value of the entity before considering liabilities and approximates the amount a willing buyer would pay for the assets of the entity immediately after the restructuring.”

Paragraph 852-10-05-10 provides that “[t]he reorganization value of an entity is the amount of resources available and to become available for the satisfaction of post-petition liabilities and allowed claims and interest, as negotiated or litigated between the debtor-in-possession or trustee, the creditors, and the holders of equity interests.”

According to Paragraph 852-10-05-10, “[s]everal methods are used to determine the reorganization value; however, generally it is determined by discounting future cash flows for the reconstituted business that will emerge from Chapter 11 and from expected proceeds or collections from assets not required in the reconstituted business, at rates reflecting the business and financial risks involved.” Paragraph 852-10-05-10 also indicates that “[r]eorganization value generally approximates fair value of the entity before considering liabilities and approximates the amount a willing buyer would pay for the assets of the entity immediately after the restructuring.” However, it may not truly represent fair value given it has been negotiated between “interested parties” in the bankruptcy process versus market participants in the context of Topic 820, Fair Value Measurement.

When estimating the reorganization value using a discounted-cash-flow (DCF) method, it is important to consider the following factors:

- Using forecast periods that extend until the prospective financial information (PFI) normalcy is reached. For example:

- Expected revenue growth rates.

- Changes in the operating cost structure/margins.

- Working/regulatory capital and capital expenditure requirements to sustain future business levels.

- Effective tax rate and specific tax considerations of the emerging entity (e.g., cancellation-of-debt and net operating loss limitations).

- Capital structure of the emerging entity based upon newly issued shares, options, and warrants and restructured debt level.

- Discount rate based on the current risk levels, capital structure, and market inputs.

- Addition of operating current liabilities to the enterprise value to arrive at a reorganization value.

- Current and forecasted economic and industry conditions.

- Impact of divestitures or other transactions should be separately valued and added back to the operating value.

Given the potential significant impact COVID-19 may have on prospective cash flows of a particular company and industry, it is recommended that various probabilistic scenarios and sensitivities of key value drivers over time be analyzed to arrive at the well-thought-out reorganization value, given the level of uncertainty that exists in today’s environment. Furthermore, when estimating the reorganization value, it is important that the preceding factors be considered based on the facts and circumstances that are known or knowable at the valuation date.

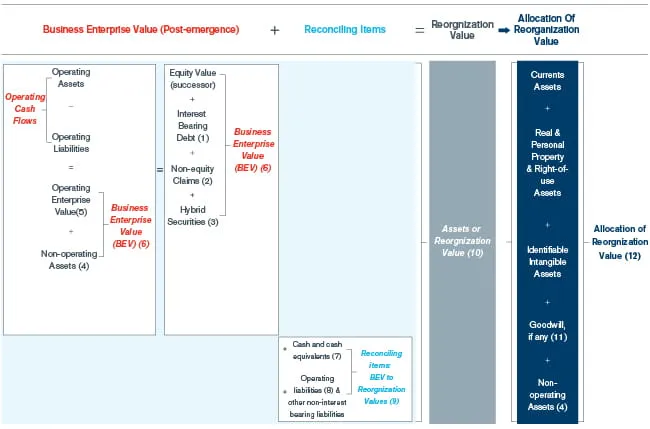

Reorganization value can be stated either as a range or a single-point estimate. A range is typically provided given sensitivities of key value drivers consistent with the entity’s emergence from bankruptcy. However, a single-point estimate will be needed to apply fresh-start reporting. A generally accepted valuation methodology of determining a company’s business enterprise value (BEV), or enterprise value, is typically used to derive the reorganization value. BEV represents the value of the underlying operations of a company, equates to the components of invested capital (i.e., long-term capital, including interest-bearing debt and equity capital). Adjustments are considered and made to the BEV, as appropriate, from a consistency perspective, such as the current and long-term non-interest-bearing liabilities, and the value of nonoperating or noncore assets to arrive at the reorganization value.

To apply fresh-start reporting, Paragraph 852-10-45-20 requires that “[t]he reorganization value of the entity shall be assigned to the entity's assets and liabilities in conformity with the procedures specified by Subtopic 805-20. If any portion of the reorganization value cannot be attributed to specific tangible or identified intangible assets of the emerging entity, such amounts shall be reported as goodwill in accordance with paragraph 350-20-25-2.” In other words, under fresh-start reporting, assets and liabilities for the emerging entity are recognized and measured in accordance with the business combinations guidance in Topic 805. The following steps are typically performed:

- Identify all reporting units of the emerging entity and determine their fair value, if applicable.

- Identify all assets and liabilities of the emerging entity (and the reporting units, if applicable), including intangible assets, that meet Topic 805 criteria for recognition.

- Determine the value of the assets and liabilities of the emerging entity (and if applicable, the reporting units). Topic 805 requires that most assets and liabilities be measured at fair value in accordance with Topic 820 but does provide several exceptions to the fair value measurement principle (for more information, see Paragraph 805-20-30-12).

- Calculate the amount of goodwill of the emerging entity (and, if applicable, each reporting unit, as appropriate), based on the residual amount of the fair value of the total assets less the fair value of the identified assets.

- If the emerging entity has multiple reporting units, perform a reconciliation of the summation of each reporting unit to the overall emerging entity.

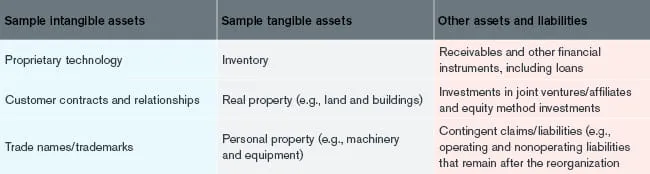

A sample listing of assets and liabilities to be considered and listed as fair value are presented in the chart below titled “Fresh-Start Emerging Fair Value Balance Sheet Items.”

Fresh-start emerging fair value balance sheet items

Typically, the total asset fair values do not exceed the reorganization value. Economic obsolescence may be observed or certain assumptions may need to be reanalyzed if the total fair value of the assets is greater than the reorganization value. This may be a result of the reorganization value not truly representing fair value, so understanding the facts and circumstances is important.

Example 2 in paragraphs 4–11 of Section 852-10-55 provides an illustration of fresh-start reporting and the related illustrative notes to financial statements. Among other things, the example illustrates the effect of the plan of reorganization on the balance sheet and associated journal entries through the reorganization process.

The following summary is a high-level overview of the reorganization process:

- The predecessor balance sheet prior to the confirmation of the reorganization plan. Negative equity (excessive leverage), triggering impairments (goodwill, other intangible assets and fixed assets), and negative working capital (liquidity issues) can often be observed.

- Actions through the Chapter 11 process. The debt is canceled, restructured, or paid (i.e., a reduction of current liabilities and long-term debt), and certain noncore assets or operations are sold (i.e., reduction of fixed assets). Normal operations and cash receipts and payments are also reflected within the financial statements.

- After the approval of the reorganization plan and emergence through fresh-start reporting. Adjustments to identify and determine the fair value (or, if applicable, another appropriate measurement principle specified in Topic 805, Business Combinations) of all assets and liabilities of the emerging entity are recognized. The reorganization value, less liabilities, represents the new equity of the emerging entity. The residual amount of the reorganization value that cannot be attributed to specific tangible or identified intangible assets of the emerging entity should be reported as goodwill.

- The emerging entity’s opening date balance sheet. After the preceding adjustments are made, the emerging entity has positive equity, less leverage, and more liquidity, and its assets and liabilities are stated at fair value, as appropriate. The emerging entity will also consider various accounting policies on existing and new matters relating to the emergence. Because Paragraph 852-10-45-21 provides that “[a]dopting fresh-start reporting results in a new reporting entity,” the emerging entity’s accounting policies do not have to be consistent with those of the predecessor, and the entity does not need to demonstrate the preferability of an accounting policy that differs from that of the predecessor, as would otherwise be required under Paragraph 250-10-45-2.

– Jonathan L. Jacobs, CPA/ABV, is a managing director in the Valuation Advisory Services segment at Duff & Phelps and is the firm’s Global Financial Services Leader; Andrew Probert, CA, is a managing director in the Transaction Advisory Services practice at Duff & Phelps and leader of the firm’s Global Transaction Accounting & Structuring offering; and Michael H. Dolan, Esq., CFA, is a managing director in the Valuation Advisory Services segment at Duff & Phelps, the firm’s Global Industrial Products Leader, and is the New York City leader, as well as the leader of the firm’s Latin America practice. To comment on this article or to suggest an idea for another article, contact Drew Adamek, a JofA senior editor, at [email protected].

Notes:

(1) Assumes interest bearing debt is shown gross, i.e., no cash is netted against it.

(2) Unfunded pensions, environmental liabilities; contingent liabilities, etc., to the extent they are included in the emerging entity. Care should be taken to not double count the associated cash flows with those used in the operating enterprise value derivation.

(3) Preferred stock, convertible debt, etc. to the extent present in the capital structure of the reconstituted entity post-emergence.

(4) Assets to be disposed of; prepaid pension assets; investments in unconsolidated subsidiaries; etc., and excess cash (non-operating cash), if any. See (1).

(5) Operating value of the business (continuing operations) before any non-operating assets. Typically derived by a DCF analysis.

(6) Negotiated value with creditors; typically determined with the help of a valuation specialist. Includes non-operating assets of the emerging entity.

(7) To the extent operating cash and/or excess cash was netted against debt or BEV, it is added back here. See (1) and (4).

(8) Operating liabilities may include accounts payable, accrued salaries, taxes payable, etc.

(9) Items added back to business enterprise value to derive the value of the assets of the emerging entity (reorganization value). See (7) and (8). Addbacks should be consistent with assumptions used in the BEV derivation.

(10) Aggregate asset value of the emerging entity, derived from BEV, and approved by the Court. The ASC Master Glossary defines Reorganization Value as "the value attributed to the reconstituted entity, as well as the expected net realizable value of those assets that will be disposed of before reconstitution occurs. Therefore, this value is viewed as the value of the entity before considering liabilities and approximates the amount a willing buyer would pay for the assets of the entity immediately after the restructuring.”

(11) Represents excess reorganization value, determined as the difference between the reorganization value and the sum of the values of the post-emergence assets of the reconstituted entity measured in accordance with ASC 805 (generally at fair value). On rare occasions, this can be a deficit.

(12) The reorganization value is allocated to the post-emergence assets of the reconstituted entity following the principles of ASC 805 (generally measured at fair value).

This article original appeared in Journal of Accountancy, December 2020. ©2020 Association of International Certified Professional Accountants. All rights reserved. Used by permission.